If you were injured in a car accident in California, you may be eligible to pursue financial compensation for emergency medical bills, lost occupational wages, and physical pain and suffering through a licensed California personal injury attorney.

The average car accident settlement in California ranges from $6,150 for minor soft-tissue injuries to upwards of $41,000 for severe fractures, according to historical data and California Highway Patrol (CHP) SWITRS collision reports.

Key legal factors to keep in mind:

- Statute of Limitations: California law imposes a strict two-year deadline from the collision date to file a formal lawsuit under CCP § 335.1.

- Pure Comparative Negligence: Traffic victims can recover proportional damages from the at-fault party even if they share partial fault for the intersection crash.

- Case Outcomes: The state-specific statistics provided on this CaseCompass portal reflect historical insurance settlement patterns and do not guarantee future case results.

California Case Strategy (Featured Video)

Learn how California's Pure Comparative Negligence impacts your final settlement, and why insurers often dispute medical severity to lower multipliers.

⚖ Law Change: AB 1107 (Effective January 1, 2025)

California raised its minimum bodily injury liability requirement from $15,000/$30,000 to $30,000/$60,000. This doubles the minimum coverage available to injury victims when the at-fault driver carries only the state minimum. If you were in an accident before January 1, 2025, the old minimums apply.

California Car Accident Laws at a Glance

- Statute of Limitations

- 2 years

- CCP § 335.1

- Fault Rule

- Pure Comparative Negligence

- Li v. Yellow Cab Co. (1975)

- Min. Liability Coverage

- $30,000/$60,000

- CVC § 16056 (AB 1107)

Key Numbers

| Metric | Value | Source |

|---|---|---|

| Average ER visit cost — Los Angeles County | $4,100 | HCUP (hcupnet.ahrq.gov) |

| Average weekly wage — California | $1,620 | BLS (bls.gov) |

| Minor injury settlement range | $6,150–$14,350 | Statewide historical data |

| Moderate injury settlement range | $14,350–$24,600 | Statewide historical data |

| Severe / catastrophic injury range | $24,600–$41,000+ | Statewide historical data |

| California statute of limitations | 2 years | CCP § 335.1 |

| Min. liability coverage (post-AB 1107) | $30,000/$60,000 | California Vehicle Code § 16056 |

| CA uninsured driver rate | ~16.6% | Insurance Research Council |

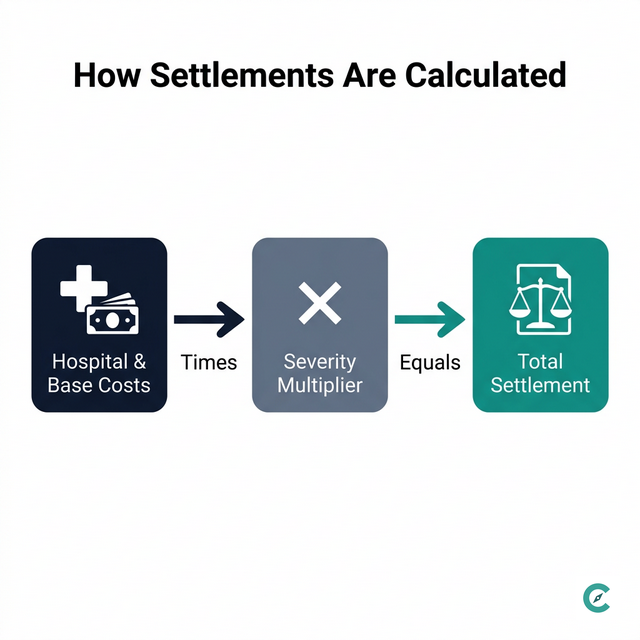

Historical Settlement Multipliers by Injury Severity

California personal injury settlements have historically been calculated by multiplying total documented medical costs by a severity multiplier. As shown in the settlement calculation diagram below, this base amount is scaled depending on the severity of the injury. These figures reflect observed patterns in settled cases — they are not a prediction or guarantee of what your case will settle for.

| Injury Type | Multiplier | Examples |

|---|---|---|

| Minor | 1.5x–3.5x | Whiplash, soft tissue strains, minor bruising |

| Moderate | 3.5x–6x | Fractures, herniated discs, surgery required |

| Severe / Catastrophic | 6x–10x+ | TBI, spinal cord injury, permanent disability, wrongful death |

Frequently Asked Questions

How long do I have to file a car accident lawsuit in California?▼

California gives you 2 years from the accident date to file a personal injury lawsuit under CCP § 335.1. If a government vehicle was involved, you may have only 6 months to file a government tort claim under California Government Code § 911.2. Missing either deadline permanently bars your claim. Contact an attorney within 30 days to preserve evidence.

What is California's Pure Comparative Negligence rule?▼

Under Pure Comparative Negligence, your compensation is reduced by your percentage of fault — but you can recover even if you were 99% responsible. If a jury finds you 40% at fault on a $200,000 claim, you recover $120,000. Insurance companies use this rule aggressively to inflate your fault percentage during settlement negotiations.

What is the new California minimum car insurance requirement in 2025?▼

California Assembly Bill 1107, effective January 1, 2025, raised minimum bodily injury liability coverage from $15,000/$30,000 to $30,000/$60,000 per person/per accident. This is the first increase in California's minimum coverage requirement in decades. Uninsured/underinsured motorist coverage minimums increased proportionally.

What is the average car accident settlement in California?▼

California settlements vary significantly by injury type and the specific facts of each case. Historically, minor injuries (soft tissue, whiplash) have settled in a range of 1.5x–3x total medical costs, moderate injuries (fractures, surgery) in a range of 3x–6x, and severe or catastrophic injuries above 6x in some cases. These are observed historical patterns, not predictions. Your outcome will depend on liability, available insurance coverage, evidence, and other case-specific factors. Consult a licensed California attorney for an evaluation of your specific situation.

Should I accept the insurance company's first offer in California?▼

No. First offers are almost always made before you reach Maximum Medical Improvement (MMI) — the point when doctors determine the full extent of your injuries. Settling early permanently waives your right to future compensation for ongoing treatment, lost earning capacity, or worsening conditions. Have a licensed California attorney review any offer before signing a release.

Does California's comparative negligence law apply to pedestrians and cyclists?▼

Yes. Pure Comparative Negligence applies to all personal injury claims in California, including pedestrian and bicycle accidents. A pedestrian who was jaywalking can still recover compensation proportional to the driver's fault. A cyclist without a helmet may have fault assigned for any head injuries, but still recovers for all other damages. There is no minimum fault threshold that bars recovery in California.

How do I know if an insurance settlement offer is fair in California?▼

An offer is generally too low if: it comes before you've reached Maximum Medical Improvement (MMI); it doesn't account for future medical costs or lost earning capacity; it uses a multiplier below 1.5x your documented medical bills for soft-tissue injuries; or the adjuster cannot explain how they calculated the amount. Under California Insurance Code § 790.03, insurers have a duty of good faith. An attorney can review any offer for free and advise whether to counter.

Can I reopen a car accident settlement in California after signing?▼

No — once you sign a full and final release in California, your claim is permanently closed. That is why you must wait until Maximum Medical Improvement (MMI) before settling. Rare exceptions exist for cases involving fraud or misrepresentation, but courts rarely overturn signed releases. Never sign a release under time pressure or before your treating physician has determined your injuries have stabilized.

California Cities with Verified CaseCompass Coverage

Each city below has a verified partner attorney who reviews local data on this platform and receives matched leads for their area exclusively.

Los Angeles Metro

Content verified by a California-licensed attorney

More California cities coming soon

Partner attorneys must meet all CaseCompass eligibility criteria before their city hub goes live.

Sources & Citations

- [1] California CCP § 335.1 — Statute of Limitations ↗

- [2] California Vehicle Code § 16056 — Min. Insurance (AB 1107) ↗

- [3] California AB 1107 — Full Bill Text ↗

- [4] CHP SWITRS — California Traffic Crash Data ↗

- [5] HCUP — Emergency Department Cost Data ↗

- [6] BLS — Occupational Employment Statistics ↗

- [7] California Dept of Insurance — Auto Guide ↗