Fuente original: Our Legal Team — Los Angeles Hit-and-Run Accident Lawyers

Si el conductor huyó, reporta el choque de inmediato y abre tu reclamo UM/UIM; en California todavía puedes buscar compensación aunque nunca identifiquen al responsable.

Find out if you have a case in Los Angeles

⚡ Free · No Obligation

See If You Qualify in 60 Seconds

Step 1 — Select accident type

What type of accident were you in?

Puntos clave

- 1.El reporte policial temprano es clave para UM/UIM.

- 2.Tu propia aseguradora negocia como parte opuesta del reclamo.

- 3.La documentación médica continua define el valor del caso.

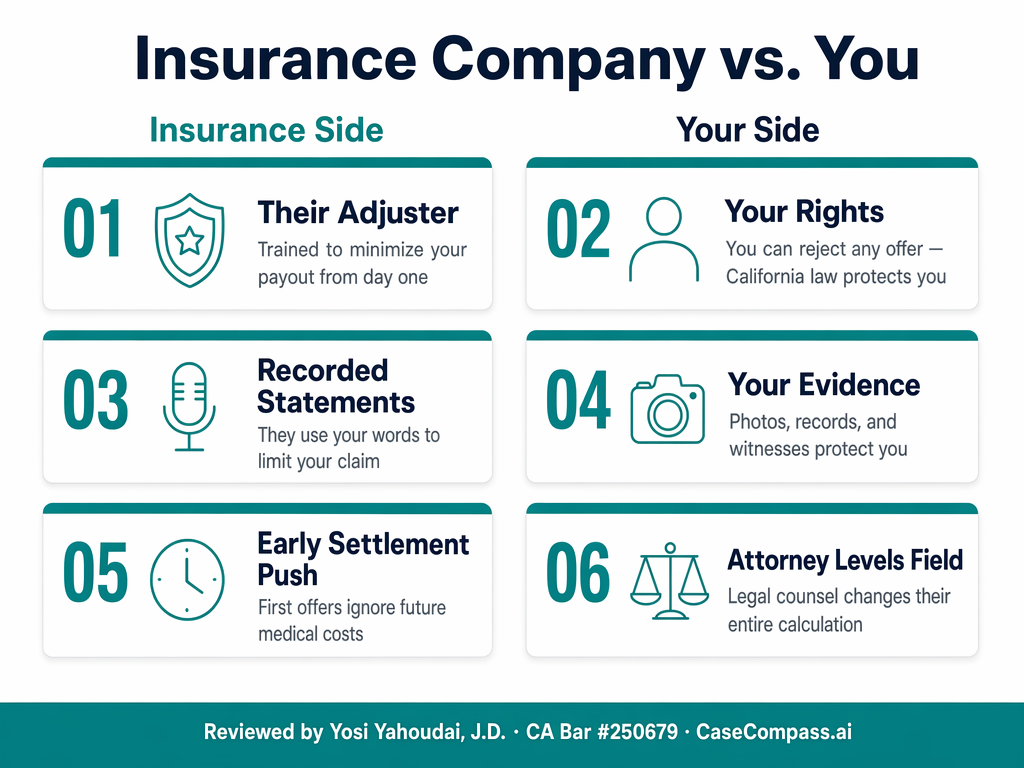

1. Why Your Own Insurer Is Not Your Ally in a UM Claim

2. The UM Arbitration Right Most Victims Never Use

3. The Recorded Statement Mistake That Kills Claims

4. What We Do the Moment You Retain Us

Not sure if your offer is fair?

Answer 3 questions to see what your case may be worth — free, no obligation.

Start Free Case Review →Preguntas frecuentes

Can I get compensation if the hit-and-run driver is never found in California?

Yes. California's mandatory UM coverage (Insurance Code § 11580.2) explicitly covers accidents caused by unknown or unidentified drivers. As long as you have a police report and UM coverage on your policy, you can file a claim and recover compensation for medical bills, lost wages, and pain and suffering — regardless of whether the driver is ever identified.

What is uninsured motorist coverage and do I have it in California?

Uninsured motorist (UM) coverage pays for injuries when the at-fault driver has no insurance or flees. California requires every insurer to offer it under Insurance Code § 11580.2. It is included by default unless you signed a written waiver. Check your declarations page to confirm your current UM limits.

What should I do if I witnessed the hit-and-run but the victim did not?

Contact the LAPD non-emergency line and provide your witness account. You can also contact the victim's attorney directly — your statement about the vehicle description, direction of travel, and driver appearance can be critical evidence in the UM claim and any subsequent criminal investigation. California has witness protection provisions for hit-and-run cases.

How long do I have to file a hit-and-run insurance claim in California?

Notify your insurer within 24–72 hours under your policy terms. The civil lawsuit deadline is 2 years from the accident date under CCP § 335.1. If the driver is identified later, you have 2 years from identification to sue directly. Contact an attorney within the first week to protect both tracks.

Will my insurance rates go up if I file a UM claim in California?

California Proposition 103 restricts insurers from raising rates on not-at-fault drivers. Filing a UM claim after a hit-and-run should not result in a premium increase. Confirm this with your insurer before filing, but do not let that concern prevent you from claiming the compensation you are entitled to.

Fuentes y citas

- California UM/UIM — [Insurance Code § 11580.2](https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=11580.2.&lawCode=INS)

- California Hit-and-Run Law — Vehicle Code § 20001

- California [CCP § 335.1](https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=335.1.&lawCode=CCP) — Statute of Limitations

- HCUP — Emergency Department Cost Data

Ready to find out if you qualify?

⚡ Free · No Obligation

See If You Qualify in 60 Seconds

Step 1 — Select accident type

What type of accident were you in?