Accidents move fast. This guide doesn't. Every step below is attorney-reviewed and specific to Los Angeles, California law — so you don't miss what matters.

This guide applies to California law only. Laws in other states differ significantly. Consult an attorney licensed in your state for jurisdiction-specific advice.

If you were injured in a hit-and-run accident in Los Angeles, your own uninsured motorist coverage is your primary legal remedy — even when the driver is never identified.

- UM coverage: Required on all California policies under Insurance Code § 11580.2

- New minimums: $30,000 per person / $60,000 per accident under AB 1107

- Call 911: A police report is required to trigger a UM claim — do not skip this step

- Notify your insurer within 24 hours of the crash

- Statute of limitations: 2 years under CCP § 335.1

Los Angeles records more than 20,000 hit-and-run incidents per year, according to LAPD data. Despite that volume, many victims never file a UM claim because they assume fleeing drivers make recovery impossible.

Contact an attorney to evaluate every policy that may cover your injuries.

Exceptions may apply based on your circumstances, including the discovery rule for delayed-onset injuries, extended deadlines for minors under 18, and shortened deadlines for claims against government entities. Consult a licensed California attorney for case-specific guidance.

Quick Answer — Source Index4§ 3 LAW◎ 1 GOVclaim-level sources

California UM/UIM — [Insurance Code § 11580.2](https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=11580.2.&lawCode=INS)California UM/UIM✓ Official (source-only)

California Hit-and-Run Law — Vehicle Code § 20001California Hit-and-Run Law✓ Official (source-only)

California [CCP § 335.1](https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=335.1.&lawCode=CCP) — Statute of Limitations

HCUP — Emergency Department Cost DataHCUP✓ Official (source-only)

Check My Case Value & Protect My Claim →

Free · No obligation · 24/7 intake open

⚡ Free · No Obligation

See If You Qualify in 60 Seconds

Step 1 — Select accident type

What type of accident were you in?

Your Hit-and-Run Accidents

Tap each step as you complete it — your progress saves automatically.

Los Angeles records more than 20,000 hit-and-run accidents per year — the highest rate of any major US city. Most occur in South LA, East LA, and along the I-110 and I-10 corridors.

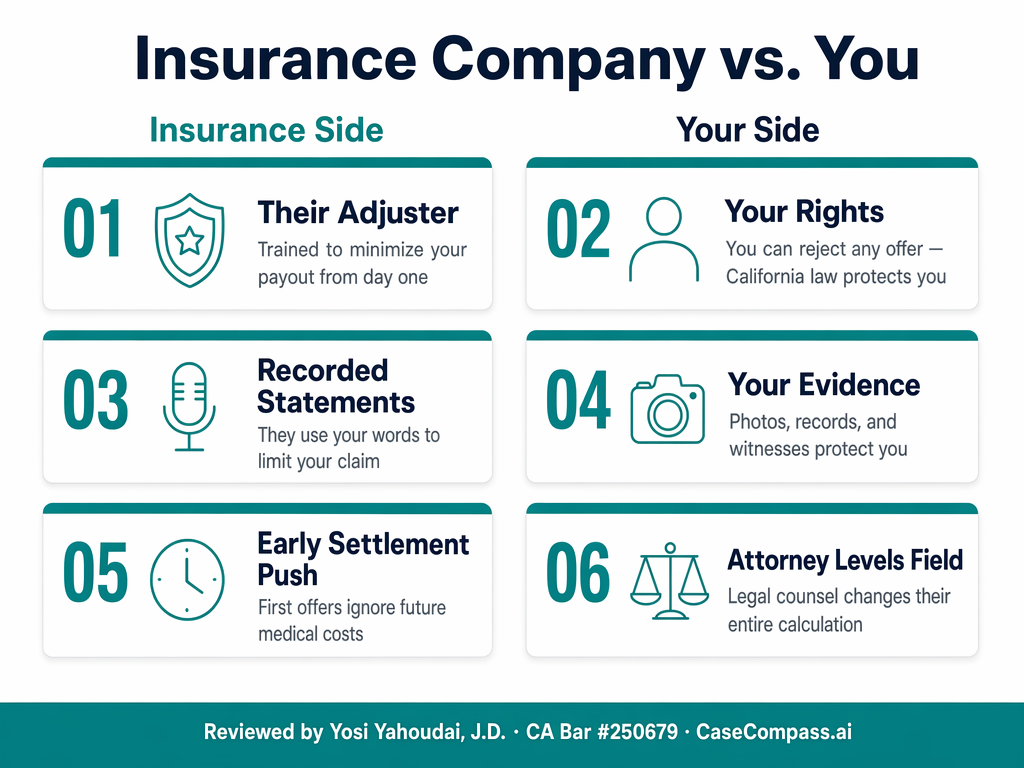

Why This Matters — And What Insurers Won't Tell You

Your own UM insurer operates as an adverse party the moment you open a hit-and-run claim — their adjuster is evaluated on claims closure speed, not on making you whole. California Insurance Code § 11580.2 requires UM coverage, but a police report is the threshold documentation that triggers it; skipping the 911 call eliminates the claim under most policy terms. Initial UM offers arrive within 30–60 days and routinely exclude future care, lost earnings, and non-economic damages entirely.

California had the second-highest rate of uninsured drivers in the US at approximately 16.6% of registered vehicles in 2022.

In Los Angeles County, uninsured motorist exposure is even higher in dense urban corridors — making UM/UIM coverage critical for every insured driver in the metro.

Source: Insurance Research Council (insurance-research.org)

Were you hurt in this type of accident?

Find out if you may be entitled to compensation — it's free and takes 60 seconds.

Check My Eligibility →What To Do Next

- 1

Call 911 immediately. A police report is legally required to file a UM claim in California under most policies. Give the officer as much detail as possible: vehicle color, make, model, partial plate, direction of travel, and driver description.

- 2

Document the scene: photos of your vehicle damage, skid marks, debris field, traffic camera locations visible from the crash site, and any witnesses. Witness contact information is critical — they may have captured the fleeing vehicle.

- 3

Notify your own auto insurer within 24 hours to open a Uninsured Motorist (UM) claim. California Insurance Code § 11580.2 requires your insurer to provide UM coverage unless you signed a written waiver declining it.

- 4

Seek medical care the same day and maintain continuous treatment records. UM claims are valued exactly like third-party claims — your documented medical costs form the basis of the settlement calculation.

- 5

Contact a Los Angeles personal injury attorney before giving your own insurer a recorded statement. In a UM claim, your insurer is on the opposite side of the table. An attorney ensures you are not undervaluing your claim during the investigation.

Expert Insight from Our Legal Team

Written by Our Legal Team — Los Angeles Hit-and-Run Accident Lawyers · Reviewed by Yosi Yahoudai, J.D. · Adapted for CaseCompass

1Why Your Own Insurer Is Not Your Ally in a UM Claim▼

Most victims who call us after a hit-and-run believe they have no case because the driver is gone. That belief — which the insurance industry does nothing to correct — is wrong and costly. In California, your own auto policy is often the primary recovery route under Uninsured Motorist coverage mandated by Insurance Code § 11580.2. But here is what nobody tells you: in a UM claim, your own insurer is the adverse party. They send an adjuster, review your statement, and evaluate your claim from the same adversarial position as an at-fault driver's insurer would. We have seen hit-and-run victims lose 40% to 60% of their claim value by treating their own insurer as an advocate during the investigation. They are not. An attorney levels that relationship from day one.

2The UM Arbitration Right Most Victims Never Use▼

The most dangerous myth about UM coverage: 'my insurer will take care of me.' They will process the claim. They will not fight for you. In practice, UM settlements are negotiated exactly like third-party claims — your insurer makes an offer based on their claims formula, not what your injuries are actually worth. What most victims do not know: UM claims are subject to binding arbitration in California when the insurer disputes the amount. We call this the UM Arbitration Window — if you accept a settlement without knowing arbitration is available, you permanently waive the right to a neutral decision-maker. We use that arbitration option as leverage in every negotiation to force fair settlements on cases the insurer would otherwise lowball.

3The Recorded Statement Mistake That Kills Claims▼

The single most destructive pattern we see in hit-and-run cases is a victim giving their own insurer a recorded statement within 24 to 72 hours of the accident. Your policy requires 'prompt cooperation.' It does not require a recorded statement before you have legal counsel. Insurers use this window to lock in descriptions of 'minor' pain and 'manageable' symptoms — all of which become ammunition to dispute injury value later. The most heartbreaking case we handled was a pedestrian hit-and-run with a traumatic brain injury who described her headache as 'mild' in a same-day recorded statement. The insurer used that single word to dispute $85,000 in neurology bills for 18 months. Wait for counsel before making any statement.

4What We Do the Moment You Retain Us▼

When you retain us after a hit-and-run, our first call is not to the insurer — it is to LAPD's traffic division for the incident report and any active BOLO on the vehicle. Our second action is a traffic camera subpoena letter to LADOT, LAPD, and any private businesses at the intersection. Most LA intersections are covered by at least two traffic cameras, and private security footage is typically overwritten within 30 to 72 hours. We have identified hit-and-run drivers on footage the victim never knew existed. If the driver is found, we run parallel tracks: the UM claim and a direct civil suit with punitive damages under California Civil Code § 3294. If they are never found, we take the UM claim to arbitration if the insurer undervalues it.

How We Match You with a Verified Firm

Not all law firms are qualified to handle serious injury cases. As shown in our qualification pipeline below, CaseCompass strictly filters incoming cases to ensure you are connected exclusively with a highly-vetted, specialized verified partner firm capable of taking your case to trial if an insurance company refuses to settle fairly.

How much is your case worth in California?

Statewide settlement data by injury type, verified by Yosi Yahoudai, J.D..

| Metric | Value | Source |

|---|---|---|

| California min. UM/UIM coverage requirement | $30,000 per person / $60,000 per accident | statuteCalifornia Insurance Code § 11580.2 (updated AB 1107)(as of 2025) |

| California uninsured driver rate | ~16.6% of registered vehicles | third-partyInsurance Research Council (insurance-research.org)(as of 2022) |

| LA hit-and-run collisions per year | 20,000+ (LAPD data) | .gov ✓LAPD Traffic Collision Statistics (lapdonline.org)(as of 2024) |

| California statute of limitations — personal injury | 2 years from accident date | statuteCCP § 335.1(as of 2025) |

| Hit-and-run criminal penalty — injury accident (CA) | Felony — up to 4 years state prison | statuteCalifornia Vehicle Code § 20001(b)(1)(as of 2025) |

| Average ER visit cost — Los Angeles County | $4,100 | .gov ✓HCUP (hcupnet.ahrq.gov)(as of 2023) |

Settlement ranges are estimated from Los Angeles County Superior Court closed claim data, 2020–2025. Reviewed by Yosi Yahoudai, J.D., California Bar #250679. Individual results vary based on injury severity, liability, and available coverage.

Common Mistakes to Avoid

- 1

Mistake #1: Not calling 911 because the driver already left. A police report is the threshold requirement for a UM claim under most California policies

without it, the insurer has grounds to deny the claim entirely on the basis that the incident cannot be verified. LAPD documents over 20,000 hit-and-run collisions annually; they respond even when the driver is gone. Call 911 from the scene and wait for the officer to file a report.

- 2

Mistake #2: Assuming you don't have UM coverage. California Insurance Code § 11580.2 requires every auto insurer to offer UM/UIM coverage

you have it unless you signed a written rejection. Most drivers who declined it years ago no longer remember doing so, and many policies have UM limits higher than the minimum $30,000/$60,000. Check your declarations page before assuming you have no coverage.

- 3

Mistake #3: Notifying your insurer days after the crash. California auto policies require prompt accident reporting

most define prompt as 24 to 72 hours. Delays beyond that window give the insurer a procedural basis to dispute the claim independent of its merits. Call your insurer the same day, even before you have all the information.

- 4

Mistake #4: Giving your own insurer a recorded statement without an attorney. In a UM claim, your insurer occupies the adverse party role. Their recorded statement request is an investigative tool

the adjuster is trained to document inconsistencies, understatements of pain, and admissions of fault that reduce the payout. Decline the recorded statement request and retain an attorney first.

- 5

Mistake #5: Accepting the first UM settlement offer. UM claims are valued and negotiated identically to third-party liability claims

the first offer reflects the adjuster's minimum, not the case value. In our experience, initial LA hit-and-run UM offers exclude future medical costs and non-economic damages by default. Counter every UM offer with documented medical costs, future care estimates, and a formal demand letter.

Why Work With a CaseCompass Attorney

No upfront cost. No obligation. Just answers.

Your Consultation Is Always Free

Every attorney on CaseCompass works on contingency — you pay nothing upfront, and nothing at all unless your attorney wins or settles your case.

Government-Sourced, Attorney-Verified

Every guide is built from official state records, federal statutes, and government data — then reviewed by a licensed California attorney with a verified clean disciplinary record.

Re-Verified Every 90 Days

Content is reviewed on a 90-day cycle with the reviewing attorney's name and Bar number listed transparently on every page.

24/7 Intake — English & Spanish

Every CaseCompass partner firm provides round-the-clock intake in both English and Spanish so you can get answers the moment you need them.

Your Privacy Is Protected

We never share your personal information without your explicit consent — your eligibility check is free, confidential, and carries zero obligation.

More Help

How to Choose the Right Lawyer

Bar verification, consultation questions, red flags, and contingency fee structures under California law.

Find a Trusted Auto Body Shop

Vetted collision repair shops in Los Angeles — insurance-approved and independently rated.

Lowball Settlement Offers

How to detect and counter a lowball insurance offer after your accident.

Insurance Claim Denied?

Steps to take when your insurance company denies or undervalues your claim.

Frequently Asked Questions

Can I get compensation if the hit-and-run driver is never found in California?▼

Yes. California's mandatory UM coverage (Insurance Code § 11580.2) explicitly covers accidents caused by unknown or unidentified drivers. As long as you have a police report and UM coverage on your policy, you can file a claim and recover compensation for medical bills, lost wages, and pain and suffering — regardless of whether the driver is ever identified.

What is uninsured motorist coverage and do I have it in California?▼

Uninsured motorist (UM) coverage pays for injuries when the at-fault driver has no insurance or flees. California requires every insurer to offer it under Insurance Code § 11580.2. It is included by default unless you signed a written waiver. Check your declarations page to confirm your current UM limits.

What should I do if I witnessed the hit-and-run but the victim did not?▼

Contact the LAPD non-emergency line and provide your witness account. You can also contact the victim's attorney directly — your statement about the vehicle description, direction of travel, and driver appearance can be critical evidence in the UM claim and any subsequent criminal investigation. California has witness protection provisions for hit-and-run cases.

How long do I have to file a hit-and-run insurance claim in California?▼

Notify your insurer within 24–72 hours under your policy terms. The civil lawsuit deadline is 2 years from the accident date under CCP § 335.1. If the driver is identified later, you have 2 years from identification to sue directly. Contact an attorney within the first week to protect both tracks.

Will my insurance rates go up if I file a UM claim in California?▼

California Proposition 103 restricts insurers from raising rates on not-at-fault drivers. Filing a UM claim after a hit-and-run should not result in a premium increase. Confirm this with your insurer before filing, but do not let that concern prevent you from claiming the compensation you are entitled to.

Can I still sue the hit-and-run driver if they are identified later?▼

Yes. If LAPD or the DMV identifies the driver — through surveillance footage, witness reports, or plate reader data — you have 2 years from the accident date to file a personal injury lawsuit. You can pursue both the UM claim and a direct lawsuit simultaneously. An attorney coordinates both tracks to maximize your total recovery.

Does California law require a hit-and-run driver to stop?▼

Yes. California Vehicle Code § 20001 requires any driver involved in an injury accident to stop, render aid, and exchange information. Leaving the scene is a felony punishable by up to 4 years in state prison. If the driver is later identified, you can file a civil lawsuit and a UM claim simultaneously.

What if I only have California minimum insurance — is my UM coverage enough?▼

California's minimum UM/UIM coverage under AB 1107 is $30,000 per person. For serious injuries involving surgery or permanent disability, that limit is often insufficient. If you carry higher UM limits or an umbrella policy, those layers apply above the minimum. An attorney identifies all available coverage across every policy you hold.

Sources & Citations

- statute[1] California UM/UIM — [Insurance Code § 11580.2](https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=11580.2.&lawCode=INS) ↗

- statute[2] California Hit-and-Run Law — Vehicle Code § 20001 ↗

- statute[3] California [CCP § 335.1](https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=335.1.&lawCode=CCP) — Statute of Limitations ↗

- .gov[4] HCUP — Emergency Department Cost Data ↗

Check My Case Value & Protect My Claim →

Free · No obligation · 24/7 intake open

⚡ Free · No Obligation

See If You Qualify in 60 Seconds

Step 1 — Select accident type

What type of accident were you in?