Accidents move fast. This guide doesn't. Every step below is attorney-reviewed and specific to Dallas, Texas law — so you don't miss what matters.

If you were injured in a Dallas car accident, Texas gives you 2 years to file a lawsuit under Tex. Civ. Prac. & Rem. Code § 16.003. You can recover damages only if you are 50% or less at fault.

Key facts for your claim:

- Statute of limitations: 2 years from the accident date — miss it and your claim is permanently barred

- Minimum liability coverage: $30,000/$60,000/$25,000 under Tex. Transp. Code § 601.072 — many Dallas drivers carry only the minimum

- 51% fault bar: If you are more than 50% responsible, you recover nothing under Tex. Civ. Prac. & Rem. Code § 33.001

- Call 911: A Texas Peace Officer crash report (CR-3) is required for injury claims

- Do not give a recorded statement to the other driver's insurer before consulting an attorney

Average car accident settlements in Texas range from $20,000 to $30,000 depending on injury severity. Serious injuries involving surgery regularly exceed $100,000.

Contact a Dallas car accident attorney before your first insurer call.

Quick Answer — Source Index5§ 3 LAW◎ 2 GOVclaim-level sources

Texas Statute of Limitations — Tex. Civ. Prac. & Rem. Code Ch. 16Texas Statute of Limitations✓ Official (source-only)

Texas Minimum Auto Insurance — Tex. Transp. Code Ch. 601Texas Minimum Auto Insurance✓ Official (source-only)

Texas Comparative Fault — Tex. Civ. Prac. & Rem. Code Ch. 33Texas Comparative Fault✓ Official (source-only)

TxDOT Motor Vehicle Crash Statistics 2024TxDOT Motor Vehicle Crash Statistics 2024✓ Official (source-only)

Texas Department of Insurance — Auto Insurance Consumer GuideTexas Department of Insurance✓ Official (source-only)

Check My Case Value & Protect My Claim →

Free · No obligation · 24/7 intake open

⚡ Free · No Obligation

See If You Qualify in 60 Seconds

Step 1 — Select accident type

What type of accident were you in?

Your Car Accident

Tap each step as you complete it — your progress saves automatically.

Dallas County recorded 46,257 crashes and 331 traffic fatalities in 2024, according to TxDOT — making it the deadliest county in the DFW Metroplex. With 1,389 serious injury crashes concentrated on I-35E, I-30, and US-75, car accidents are the most common personal injury claim in Dallas.

Why This Matters — And What Insurers Won't Tell You

Insurance adjusters in Dallas begin building their liability assessment within the first 72 hours — before you have retained counsel, reviewed the CR-3 crash report, or completed diagnostic imaging. That initial fault percentage shapes every negotiation that follows. Under Texas's modified comparative negligence rule, even a 20% fault assignment on a $100,000 claim reduces your recovery to $80,000 — and anything above 50% eliminates it entirely under Tex. Civ. Prac. & Rem. Code § 33.001.

Adjusters also make early settlement offers before you reach Maximum Medical Improvement. A $12,000 offer for soft tissue injuries sounds reasonable until you discover three months later that you need a cervical fusion costing $85,000. Once you sign a release, that number is final — Texas law does not allow you to reopen a settled claim.

The gap between a first offer and actual case value in Texas averages 40%–60%, according to Fielding Law's case data across 5,000+ resolved claims. Early legal counsel changes the math on every one of these decisions.

Dallas County recorded 46,257 total crashes and 331 traffic fatalities in 2024 — the highest fatality count in the DFW Metroplex.

I-35E, I-30, and US-75 account for a disproportionate share of serious injury crashes in Dallas County. Texas recorded one reportable crash every 57 seconds statewide in 2024.

Source: TxDOT Crash Records 2024

Were you hurt in this type of accident?

Find out if you may be entitled to compensation — it's free and takes 60 seconds.

Check My Eligibility →What To Do Next

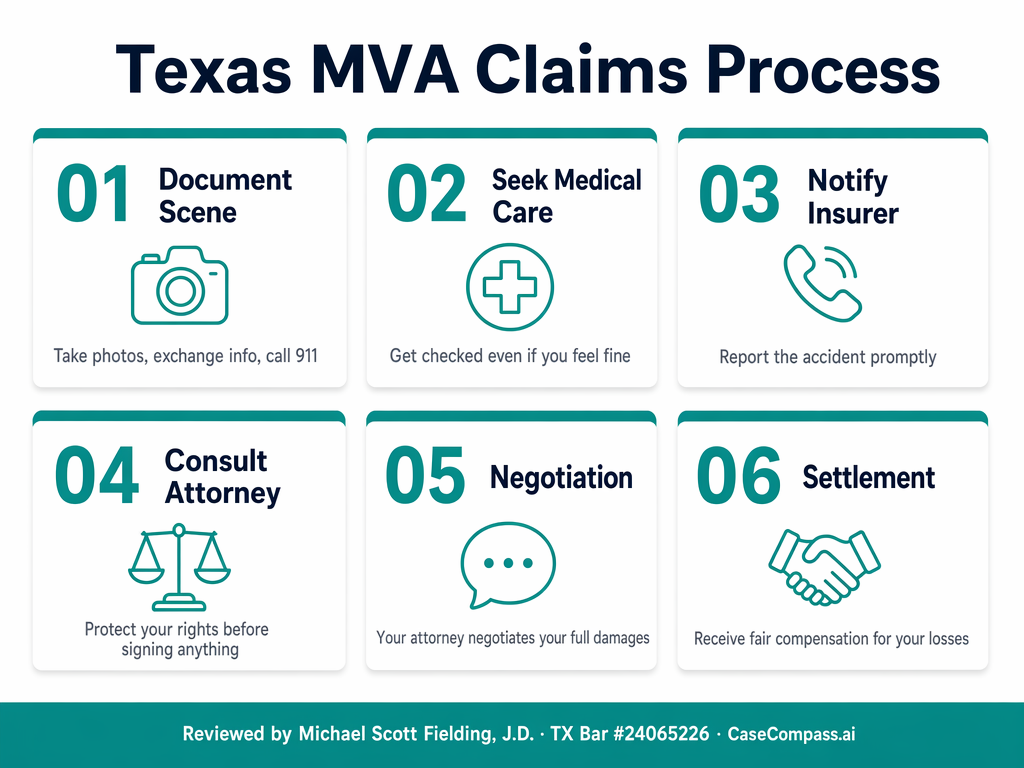

- 1

Call 911 immediately. Texas law requires reporting any crash involving injury, death, or property damage exceeding $1,000. The responding officer generates a CR-3 crash report — your insurance claim and any future lawsuit depend on this document.

- 2

Photograph everything before vehicles are moved: damage to all vehicles, your visible injuries, road conditions, traffic signals, skid marks, and vehicle positions. Take wide-angle photos from multiple directions and close-ups of each damage point.

- 3

Exchange information with all drivers: full name, driver's license number, insurance company, policy number, vehicle make/model, and license plate. Photograph their insurance card and driver's license directly.

- 4

Get names and phone numbers of all witnesses. Independent witness statements carry significant weight in fault disputes — adjusters give them more credibility because witnesses have no financial stake in the outcome.

- 5

See a doctor the same day, even if you feel fine. Adrenaline masks pain for hours. A gap of 3 or more days between the accident and your first medical visit is routinely used by Texas insurers to argue your injuries were pre-existing or unrelated to the crash.

- 6

Do not give any recorded statement to any insurance company — including your own — before consulting an attorney. Texas law does not require you to provide a recorded statement to the opposing insurer. Statements made in the first 72 hours are used verbatim to dispute injury severity throughout the claim.

Expert Insight from Our Legal Team

Written by Fielding Law · TX Bar #24065226 · Reviewed by Michael Scott Fielding, J.D. · Adapted for CaseCompass

1The Texas Coverage Gap: Why Minimum Insurance Fails After a Serious Crash▼

Texas requires $30,000/$60,000/$25,000 in liability coverage under Tex. Transp. Code § 601.072. Those numbers sound adequate until you're staring at a $85,000 surgical bill after a rear-end collision on I-30. In our experience handling thousands of Dallas-area claims, the at-fault driver's minimum policy covers barely a third of serious injury costs. The remaining gap falls on you unless your own policy carries adequate UM/UIM coverage. Most drivers discover this gap for the first time after the crash — when it's too late to change their policy. Mitchell Fielding, Managing Partner at Fielding Law, recommends every Texas driver carry at least $100,000/$300,000 in UM/UIM coverage, even though state law allows you to reject it in writing.

2PIP Coverage in Texas: The 72-Hour Safety Net Most Drivers Decline▼

Texas insurers are required to offer Personal Injury Protection, but most drivers reject it to save on premiums. PIP pays for medical bills and a portion of lost wages regardless of who caused the crash. While liability is still being investigated — and that investigation can take months — PIP provides immediate financial relief. In practice, this means the difference between starting physical therapy in week one versus waiting 4 months for the adjuster to assign fault. PIP is not a substitute for a full claim, but it buys you time. Fielding Law advises Dallas clients to accept PIP coverage. The premium increase is typically $15–$30 per month. The alternative is paying medical bills out of pocket while your claim is being processed.

3How the 51% Bar Rule Turns Insurance Disputes Into Zero-Recovery Outcomes▼

Texas follows a modified comparative fault rule under Tex. Civ. Prac. & Rem. Code § 33.001. At 50% fault, your compensation is cut in half. At 51%, it vanishes entirely. Insurance adjusters understand this threshold better than most attorneys. Their goal in the first 10 days is to build a liability narrative that pushes your fault percentage as close to 51% as possible — even on claims where the other driver ran a red light. We have seen adjusters cite failure to wear a seatbelt, speeding 3 mph over the limit, or 'failure to take evasive action' as contributing factors to inflate fault assignments. The counter-strategy: preserve every piece of evidence immediately. Dashcam footage, intersection cameras, and witness statements are the only reliable tools to challenge an inflated fault percentage.

4UM/UIM Coverage: Your Only Recourse When the At-Fault Driver Has Nothing▼

Uninsured and Underinsured Motorist coverage pays for your injuries when the at-fault driver has no insurance or insufficient coverage. Texas insurers must offer UM/UIM, but drivers can decline it in writing. In Dallas, where uninsured driver rates remain significant, declining UM coverage is one of the most consequential insurance decisions you can make. Hit-and-run crashes — where the at-fault driver is never identified — are treated as uninsured motorist claims. Without UM coverage, you have no first-party recovery path. Fielding Law has recovered millions through UM/UIM claims alone. The coverage costs $10–$40 per month depending on limits, and it may be the only thing standing between you and an unpaid $50,000 medical bill.

How We Match You with a Verified Firm

Not all law firms are qualified to handle serious injury cases. As shown in our qualification pipeline below, CaseCompass strictly filters incoming cases to ensure you are connected exclusively with a highly-vetted, specialized verified partner firm capable of taking your case to trial if an insurance company refuses to settle fairly.

How much is your case worth in Texas?

Statewide settlement data by injury type, verified by Michael Scott Fielding, J.D..

| Metric | Value | Source |

|---|---|---|

| Texas statute of limitations — personal injury | 2 years from accident date | [Tex. Civ. Prac. & Rem. Code § 16.003](https://statutes.capitol.texas.gov/Docs/CP/htm/CP.16.htm) |

| Texas minimum bodily injury liability | $50,000 per person / $100,000 per accident | [Tex. Transp. Code § 601.072](https://statutes.capitol.texas.gov/Docs/TN/htm/TN.601.htm) (updated Jan 1, 2026) |

| Modified comparative negligence threshold | 51% — exceed this and you recover nothing | [Tex. Civ. Prac. & Rem. Code § 33.001](https://statutes.capitol.texas.gov/Docs/CP/htm/CP.33.htm) |

| Average car accident settlement — Texas | $20,000 – $30,000 | ConsumerShield / KRW Lawyers (TX-specific estimates) |

| Average ER visit cost — no insurance | ~$2,600 | UnitedHealthcare / Mira |

| Settlement multiplier range | 1.5x – 5x special damages | TX TDI closed claim data, 2023–2025 |

| Dallas County total crashes (2024) | 46,257 | [TxDOT Crash Records 2024](https://www.txdot.gov/data-maps/crash-reports-records/motor-vehicle-crash-statistics.html) |

Common Mistakes to Avoid

- 1

Mistake #1: Waiting more than 24 hours to see a doctor. By the time most victims call us, 4 or 5 days have passed since the crash. The insurer's adjuster has already flagged the treatment gap. A delay of 3 or more days gives Texas insurers grounds to argue your injuries were pre-existing or caused by something other than the accident

and that argument works more often than it should. See a doctor the same day. Even an urgent care visit creates the causal medical record your claim depends on.

- 2

Mistake #2: Giving a recorded statement to the at-fault driver's insurer. Texas law does not require you to cooperate with the opposing insurer's investigation. In handling over 5,000 claims, Fielding Law has seen recorded statements made in the first 48 hours

before symptoms fully develop — used to cap injury severity for the entire life of the claim. Adjusters are trained to ask questions that minimize your injuries. Decline every recorded statement request until you have consulted an attorney.

- 3

Mistake #3: Accepting the first settlement offer. First offers in Dallas auto claims typically cover only documented ER bills and ignore future care, lost earning capacity, and non-economic damages entirely. The gap between a first offer and actual case value averages 40%–60%. Once you sign a release, the claim is closed

Texas does not allow reopening. Do not sign any release or accept any offer before reaching Maximum Medical Improvement and consulting an attorney.

- 4

Mistake #4: Assuming fault is obvious and not preserving evidence. Insurance adjusters assign fault percentages within the first 10 days, often before victims have reviewed the CR-3 crash report. Surveillance footage from nearby businesses and dashcam recordings are typically overwritten within 30–72 hours. In multi-vehicle crashes on I-35E or I-30, fault determination is rarely straightforward. An attorney can send a spoliation preservation letter immediately to prevent evidence destruction.

- 5

Mistake #5: Not understanding the 51% bar rule. Texas follows modified comparative negligence. If you are assigned even 51% fault, your recovery drops to zero

not a proportional reduction, a complete bar. Adjusters know this threshold and build their initial assessment to push your fault percentage as close to 51% as possible. Document everything and get legal counsel early to challenge any inflated fault assignment.

Why Work With a CaseCompass Attorney

No upfront cost. No obligation. Just answers.

Your Consultation Is Always Free

Every attorney on CaseCompass works on contingency — you pay nothing upfront, and nothing at all unless your attorney wins or settles your case.

Government-Sourced, Attorney-Verified

Every guide is built from official state records, federal statutes, and government data — then reviewed by a licensed California attorney with a verified clean disciplinary record.

Re-Verified Every 90 Days

Content is reviewed on a 90-day cycle with the reviewing attorney's name and Bar number listed transparently on every page.

24/7 Intake — English & Spanish

Every CaseCompass partner firm provides round-the-clock intake in both English and Spanish so you can get answers the moment you need them.

Your Privacy Is Protected

We never share your personal information without your explicit consent — your eligibility check is free, confidential, and carries zero obligation.

More Help

How to Choose the Right Lawyer

Bar verification, consultation questions, red flags, and contingency fee structures under Texas law.

Find a Trusted Auto Body Shop

Vetted collision repair shops in Dallas — insurance-approved and independently rated.

Lowball Settlement Offers

How to detect and counter a lowball insurance offer after your accident.

Insurance Claim Denied?

Steps to take when your insurance company denies or undervalues your claim.

Frequently Asked Questions

How long do I have to file a car accident lawsuit in Dallas?▼

Texas gives you 2 years from the accident date under Tex. Civ. Prac. & Rem. Code § 16.003. Miss this deadline and you permanently lose the right to sue. Claims against government entities require formal notice within 6 months — sometimes 90 days. Contact an attorney within 30 days to preserve evidence.

How much is a car accident settlement worth in Dallas?▼

Average Texas car accident settlements range from $20,000 to $30,000 for moderate injuries. Minor soft tissue injuries settle for $3,000–$15,000. Serious injuries involving surgery or permanent impairment can exceed $100,000. The average Texas jury verdict is $826,892. Your case value depends on medical costs, lost wages, and pain and suffering.

What is Texas's modified comparative negligence rule?▼

Texas uses a 51% bar rule under Tex. Civ. Prac. & Rem. Code § 33.001. If you are 50% or less at fault, your compensation is reduced by your fault percentage. If you are 51% or more at fault, you recover nothing. Insurance adjusters actively build their case to push your fault percentage above this threshold.

Should I accept the insurance company's first settlement offer?▼

No. First offers typically cover only documented ER bills and exclude future medical care, lost earning capacity, and non-economic damages. The gap between first offers and actual case value averages 40%–60%. Never sign a release before reaching Maximum Medical Improvement. Consult an attorney before responding to any offer.

Do I need a police report after a car accident in Dallas?▼

Yes. Texas requires reporting any crash involving injury, death, or property damage over $1,000. The responding officer generates a CR-3 crash report. This document is required for insurance claims and lawsuits. If police do not respond, you can file a report at any Dallas Police Department substation within 10 days.

What is the minimum car insurance required in Texas?▼

As of January 1, 2026, Texas requires $50,000 per person / $100,000 per accident for bodily injury and $40,000 for property damage under Tex. Transp. Code § 601.072. Many Dallas drivers carry only this minimum. PIP and UM/UIM must be offered but can be rejected in writing. Minimum coverage is often insufficient for serious injuries.

Can I still recover damages if I was partially at fault in Dallas?▼

Yes, as long as your fault does not exceed 50%. Texas reduces your compensation by your fault percentage under modified comparative negligence. At 30% fault on a $100,000 claim, you recover $70,000. At 51% fault, you recover nothing. An attorney can challenge inflated fault assignments from adjusters.

How much do car accident lawyers charge in Texas?▼

Most Texas personal injury attorneys work on contingency — you pay nothing upfront and no fees unless you recover compensation. The standard contingency fee is 33%–40% of the settlement or verdict. Fielding Law offers free consultations and charges no fee unless your case is won.

What should I do if the other driver has no insurance in Dallas?▼

File a claim under your own Uninsured Motorist (UM) coverage if you have it. Texas insurers must offer UM/UIM coverage, but drivers can reject it in writing. If you declined UM coverage, your options narrow to suing the uninsured driver directly. An attorney can evaluate all available coverage sources.

How long does a car accident claim take to settle in Dallas?▼

Simple soft tissue claims may settle in 3–6 months. Cases involving surgery, disputed liability, or multiple parties often take 12–18 months. Do not rush settlement before reaching Maximum Medical Improvement — early settlement permanently caps your recovery. An attorney can negotiate while you focus on treatment.

Sources & Citations

- [1] Texas Statute of Limitations — Tex. Civ. Prac. & Rem. Code Ch. 16 ↗

- [2] Texas Minimum Auto Insurance — Tex. Transp. Code Ch. 601 ↗

- [3] Texas Comparative Fault — Tex. Civ. Prac. & Rem. Code Ch. 33 ↗

- [4] TxDOT Motor Vehicle Crash Statistics 2024 ↗

- [5] Texas Department of Insurance — Auto Insurance Consumer Guide ↗

Check My Case Value & Protect My Claim →

Free · No obligation · 24/7 intake open

⚡ Free · No Obligation

See If You Qualify in 60 Seconds

Step 1 — Select accident type

What type of accident were you in?